Digital Channels

Intelligence and experience merged into one

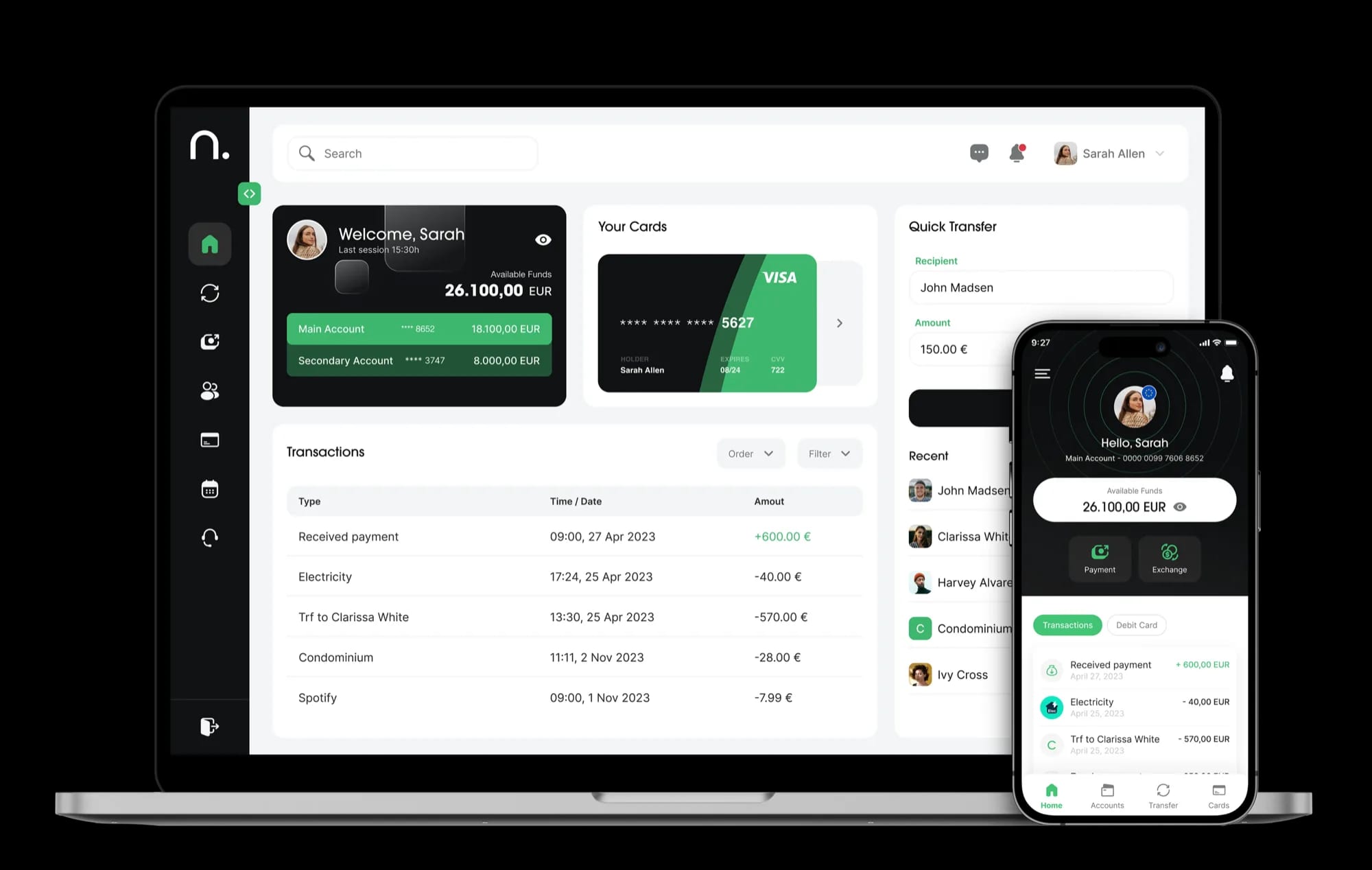

Consistent and personalised mobile and web experiences. Every interaction is powered by data and AI, delivering seamless journeys that adapt in real time.

Meet Nearsoft at FEBRABAN Tech in São Paulo, August 24–26!Meet Nearsoft at FEBRABAN Tech in São Paulo, August 24–26!

Learn MoreNearsoft transforms your digital channels into seamless, personalised journeys, powered by data and AI that adapt in real time, built for the world's most regulated environments.

ISO/IEC 27001 certified and DORA-aligned for the resilience, continuity, and third-party risk requirements regulated institutions expect.

Intelligence and experience merged into one

Consistent and personalised mobile and web experiences. Every interaction is powered by data and AI, delivering seamless journeys that adapt in real time.

See what matters first

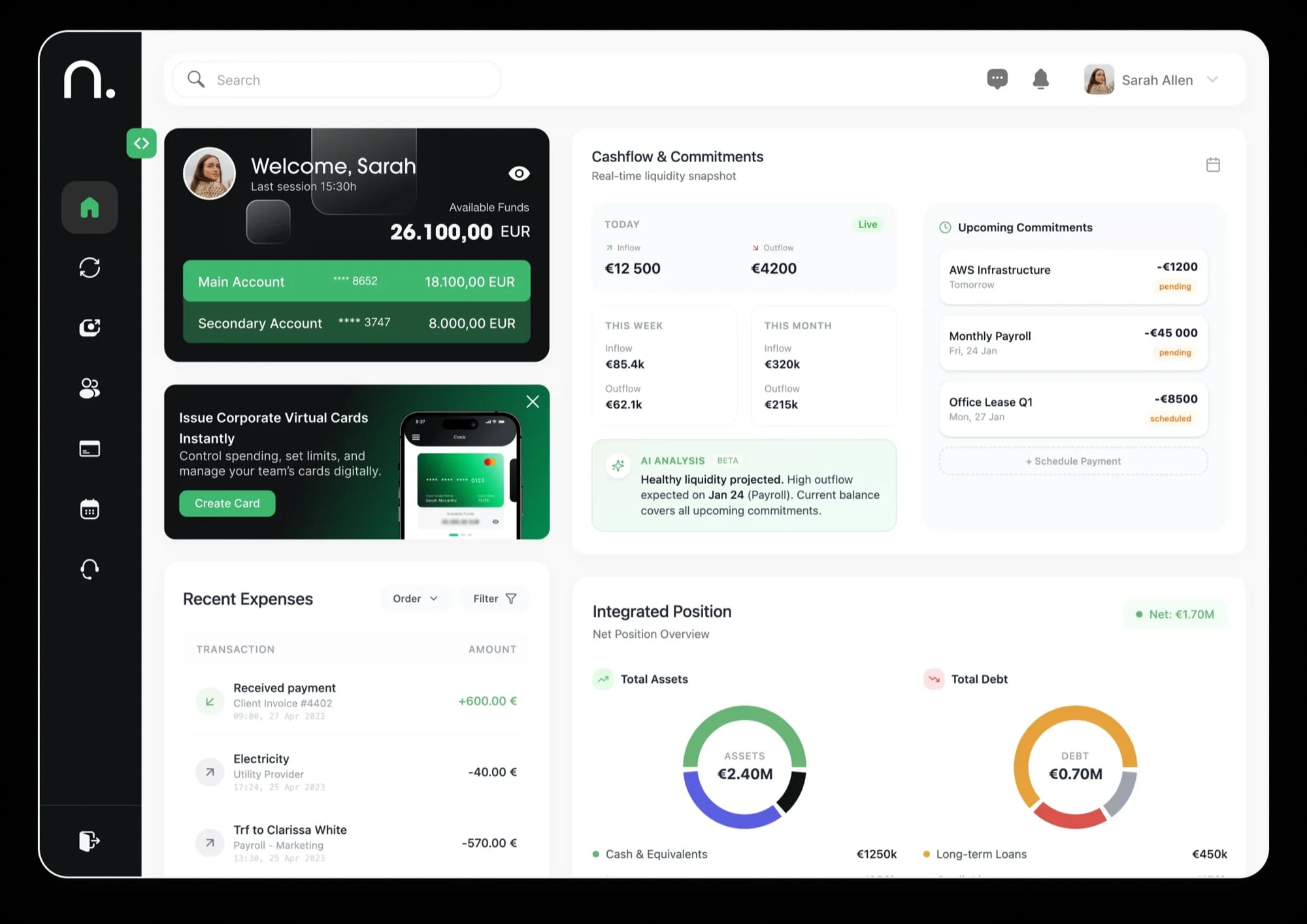

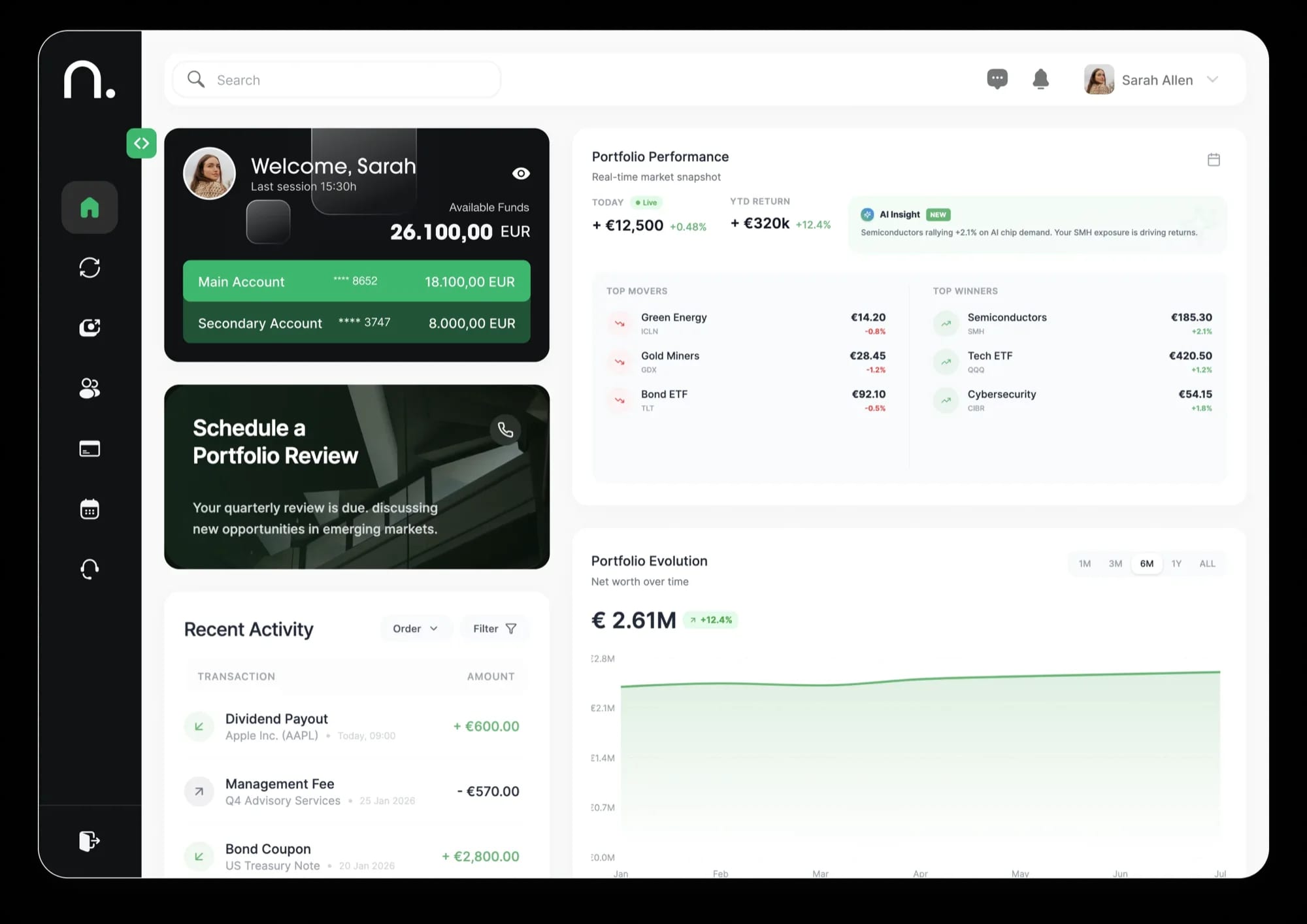

Insights that power artificial intelligence, drive personalisation across digital channels and support confident, data-driven decisions.

Turn every interaction into opportunity

AI connects intent across web, app and conversational channels, enriches CRM profiles and creates qualified leads for the right team to act on.

The connective intelligence behind it all.

Trained on your data and running inside your environment, it works across every digital channel, turning real events in each customer's financial life into timely, compliant, on-brand outreach.

A composable, core-agnostic digital banking platform, from core to intelligence, in a single architecture. Connect to any core banking system, add web, mobile, CRM, data and AI capabilities as you grow, and scale without forced migrations or rebuilds. Built to evolve with your business, not against it.

AI

Turn everyday banking operations into autonomous workflows you can trust, connected to your systems, running on your own infrastructure, and governed end to end.

Business

Internet banking, mobile, onboarding, CRM and self-service as standalone products, not a monolithic suite. Adopt one, adopt all, and add the rest whenever your roadmap calls for it, connected to your entire application landscape.

Integrations

One integration layer for your entire application landscape. Core, channels, switches and third parties talk in real time through events and open APIs, orchestrated centrally, so change in one system never breaks another.

Data

An event-sourced data layer that captures every interaction into a governed data lake and turns it into a real-time 360º view of each customer, the same data that powers analytics today and feeds the AI layer above.

Core Banking

Core-agnostic by design. We connect to the core banking system you already run, and to everything around it, so you modernize on top of what works instead of replacing it. Any core, no lock-in.

Banking products that think, adapt, and grow with your customers.

Turn daily transactions into moments that build loyalty, real-time notifications, smart insights, and frictionless money movement.

Enable complex business banking with multi-level approvals, entitlements, and straight-through workflows, built for high volume and control.

Portfolio insight, personalized guidance, and seamless investing, delivered through digital and advisor-led journeys.

Start relationships instantly. Onboard customers in minutes, without operational drag or manual bottlenecks.

News from our projects, research, and teams across regulated markets.

Nearsoft will be exhibiting at FEBRABAN TECH 2026. From August 24 to 26, we will be at Distrito Anhembi in São Paulo to showcase how we help financial institutions accelerate innovation, embed AI into their digital evolution and launch new experiences with greater agility, securi…

Read moreNEARSOFT was present at Building The Future 2026 in Lisbon on the 12th of March, one of Portugal’s leading events dedicated to innovation, technology, and digital transformation. The event brought together global leaders, companies, and policymakers to discuss the future of artif…

On World Quality Day, we’re excited to announce that Nearsoft has officially achieved the ISO/IEC 27001:2022 certification, issued by Prescient Security , a global recognition of our commitment to information security, trust, and excellence. This milestone reflects the dedication…

Our CEO, Pedro Camacho , recently took the stage at the Fintech Festival Tanzania 2025 to share Nearsoft ’s vision for global expansion. His message was clear: the future of digital banking must be inclusive, partner-driven, and globally scalable, without compromising quality or …